Logitech (LOGI) is enjoying a strong start to fiscal 2015. The company posted impressive results in the first quarter, exceeding expectations. The company came up with impressive results on the back of strong retail sales growth. Management is confident of delivering better results in the future as Logitech is well-positioned financially, which is evident from its robust sales growth for the fifth consecutive quarter. It is adopting several strategies and bringing in new products to hold a unique image among the customers. With the future looking bright, there is lot more in Logitech. Let us find out what more the company has to offer to investors.

Results and beyond

In the recently reported quarter, Logitech posted a 1% increase in sales to $484 million. it led the company to see good improvement in the non-GAAP net income. Logitech posted Non-GAAP net income of $44 million. Logitech also saw noticeable growth in the EPS. The company posted EPS of $0.23, which is better than $0.07 per share as compared to a year ago.

Logitech entered the new fiscal year in great fashion. The stock had been impressive due to the consistent sales growth over the period. Logitech kept its commitments and again posted considerable growth in sales for the fifth consecutive quarter. The company is seeing robust growth in its core categories such as PC gaming, tablets, mobile speakers, and other accessories. Following the terrific results, Logitech posted an upbeat outlook which helped it to further gain traction on the stock market.

Innovation in focus

Logitech is focusing on innovations and adding new products to strengthen its product portfolio. It is exploring other venues to seek profitability. It has recently announced that it is bringing in four new products home automation product compatibility. This will polish its leadership in universal remotes.

One of these new products is the New Harmony. This is rapidly gaining recognition due to its special features. It gives the customer an easy access and control over a wide library of entertainment and home automation devices, all from one centralized control system. With Harmony, Logitech is focusing on simplifying home entertainment.

Moving on to its core business, Logitech is also making new additions in its PC gaming segment. According to its latest announcements, Logitech has recently brought in a new gaming keyboard: Logitech G910 Orion Spark RGB Mechanical Keyboard. It is claiming to have launched most advanced mechanical gaming keyboard in the world.

What attracts customers is that it comes loaded with exclusive new Romer-G™ mechanical switches, offering 25% faster actuation than any other mechanical switch. It also has improved durability and intelligent illumination. This keyboard is expected to gain more traction in the market and even the management had stated that the gamers like the new switches that Logitech introduced with its new keyboard.

Tablet focus

Logitech is also focusing on the tablet accessory market with a new Samsung offering. It has also introduced Logitech type-S, which is a protective keyboard case for the Samsung Galaxy Tab S.

Logitech is also seeing good opportunities in the video collaboration. Its product portfolio for this is strong. It is seeing good demands for high quality audio and video. With such a demand, Logitech is expecting an increase in the shipment of its offerings for the low price, high quality video collaboration solutions in fiscal 2015.

Conclusion

Moving to the fundamentals, Logitech is reasonable with a trailing P/E of 27.72. But the forward P/E of 12.62 shows slow, yet steady earnings growth. The profit margin is also satisfactory with 4.53%. But for the next five years, the earnings are declining at a CAGR of -3.2% which is an indication that its long-term prospects are not strong. But the company is gaining good market share on the back of its innovations and new products in the market. Considering the facts and ratios, investors seeking short term gains should definitely include Logitech in their portfolio, as it stock looks perfectly in shape for the near future.

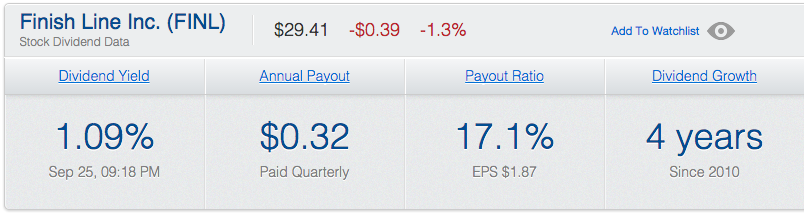

Finish Line Inc Misses Q2 Estimates; Shares Sink (FINL)Before the opening bell on Friday morning, Finish Line Inc. (FINL FINL’s Earnings in Brief Finish Line reported second quarter revenues of $466.88 million, up from last year’s Q2 revenues of $436.03 million. Net income for the quarter came in at $26.16 million, or 54 cents per diluted share, which is essentially flat with last year’s Q2 figures of $26.5 million, or 54 cents per share. FINL’s Q2 results missed analysts’ estimates of 60 cents EPS on revenues of $477.61 million. For FY2015, Finish Line expects comparable store sales to be up mid single digits and earnings per share to increase in the high single to low double digit range.CEO Commentary FINL chairman and CEO Glenn Lyon had the following comments: "Our second quarter results fell short of our expectations due to softness within elements of our basketball offering while our running business was up mid single digits driven by casual and performance styles. We are confident that we can reaccelerate sales trends in basketball by working closely with our brand partners to improve our assortments. In combination with our market leadership position in running, advanced omnichannel capabilities and growing business relationship with Macy's, this will fuel sustainable sales and earnings growth over the long-term." FINL’s Dividend Finish Line most recently paid a dividend on September 15. We expect the company to declare its next quarterly dividend of 8 cents in the coming month. Stock Performance FINL stock was down $2.41, or 8.19%, in pre-market trading. YTD, the stock is up 4.48%. FINL Dividend SnapshotAs of Market Close on September 25, 2014 Click here to see the complete history of FINL dividends. Wednesday, September 24, 2014Android Switchers Could Drive Impressive iPhone 6 SalesUntil Apple (NASDAQ: AAPL ) launched its lineup of larger smartphones with the 4.7-inch iPhone 6 and the 5.5-inch iPhone 6 Plus on Friday, Google's (NASDAQ: GOOG ) Android benefited from Apple's absence in the hot market for large smartphones and phablets. But now, with Apple's latest-generation iPhones giving Android users an excellent alternative to large phones like the Android-powered Samsung Galaxy S5, the Galaxy Note lineup, and the LG G3, Apple is likely to snap up users who decide to switch over to iOS from Android.  iPhone 6. Image source: Apple. Samsung's loss, Apple's gain As AppleInsider notes, Cowen & Company analyst Timothy Arcuri "also believes that the iPhone 6 and iPhone 6 Plus will target high-end Android switchers."  iPhone 6 and iPhone 6 Plus. Image source: Apple. Solid benchmarks Keep in mind that Apple was able to pull these feats off in spite of the fact that its newest iPhones are thinner than ever before -- and thinner than competitors. Of course, given the premium price point that Apple sells its iPhones for, all of these performance achievements are expected. Even so, it's clear that Apple has made quite an entrance into the growing market of large screen-size smartphones -- an entrance that will undoubtedly convince some Android users to switch over to Apple's iOS ecosystem. Apple CEO Tim Cook boldly told The Wall Street Journal in an interview after its iPhone media event earlier this month that the iPhone 6 and 6 Plus would spark "the mother of all upgrades" and that he expects Android users to switch.  iPhone 6. Image source: Apple. Apple wants to capitalize on the opportunity to convince Android users to switch over to iOS with the iPhone 6 and 6 Plus as much as possible. In a move to help Android users make the switch to iOS, Apple released a detailed support document that explains how they can move their data from their Android devices to the iPhone. Growing Apple's current annual iPhone sales level of 164 million units won't be easy, but tapping into the market for larger smartphones that was, until now, dominated by Android will certainly help. Apple Watch revealed: The real winner is inside Tuesday, September 23, 2014L.A.'s Sunset Strip Goes Corporate: Whisky a Gone Gone

Saturday, September 20, 2014Meridian Contrarin Fund Second Quarter Letter

In the letter, President Daivd Corkins talked about the rise in the S&P 500 and the Russell 2000. He also talked about the Federal Reserve's accomodative policy, the improvements in the housing market, employment and manufacturing. Letter To Partners: Dear Shareholder, During the year ending June 30, 2014, the S&P 500 and the Russell 2500 (small and medium sized companies) returned over 24.6% and 25.5%, respectively. Continued accommodative Fed policy, along with improvements in housing, employment and manufacturing were all supportive macro-economic factors that drove an overall increase in earnings and valuation for the indices. The current low interest rate environment and the longer-term trends of globalization and technology-enhanced productivity form a powerful recipe for cash-flow generation and capital markets activity. In addition to helping drive strong U.S. equity market returns over the past few years, these market forces are contributing to positive capital flows into equities, increased corporate debt and equity issuance – and a healthy pickup in merger and acquisition activity (M&A). M&A has traditionally been a barometer of overall CEO confidence, and, according to Bloomberg, the dollar value of global M&A during the first half of 2014 increased 89% over the same period a year ago, suggesting investors are not alone in their sanguine view of the future. While optimism abounds for the market as a whole, it is worth a reminder that the stock market is not the economy. Underlying economic data may not be as robust as stock prices would suggest. First half 2014 U.S. GDP growth is set to come in around 1% (2% annualized) and significant slack remains in the labor market. Reforms and deleveraging in Europe create the specter of deflation in the region and widespread geopolitical tensions remain at the top of the list of overall global risks. At Arrowpoint and the Meridian Funds (Trades, Portfolio), we are not economic prognosticators, nor traders; our value-add is fundamental research first and foremost. We seek to combine attractive asymmetric risk/reward investments within a risk-managed equity portfolio. The intended outcome is to preserve capital in volatile market environments without sacrificing upside participation in up markets. As our first year as Investment Adviser to the Meridian Fund family comes to a close, we are excited about enhancements that have been made to the client service side of the business. This includes the establishment of quarterly commentaries and a new website with substantially improved data and functionality. Please visit us at www.meridianfund.com or Arrowpoint Partners at www.ap-am.com for more information on our strategies. On behalf of all the Meridian and Arrowpoint team members, thank you for your continued trust, confidence and investment in the Meridian Fund family. Respectfully, David Corkins President Meridian Contrarin Fund portfolio performance On September 5, 2013, we began managing the Meridian Growth Fund. It is our distinct honor to take the helm of this venerable fund, which was founded by Richard Aster nearly 30 years ago. Through rigorous fundamental research, disciplined portfolio construction and a focus on managing risk before reward, we hope to expand upon Meridian Growth Fund's legacy. We will use the same process and philosophy that served us well managing another mutual fund for 7 years. Namely, our investment philosophy is centered on four key tenets: Employ fundamental research to identify high-quality growth businesses with predictable and recurring revenues, high returns on invested capital and attractive risk-reward profiles. Build a durable portfolio that first and foremost protects capital in tough, turbulent markets and secondarily keeps up with the broader market in bull market environments. Always think about risk before reward. Almost 30 years of combined experience in small- and mid-cap markets have taught us the importance of sidestepping the landmines and pitfalls that trip up many other investors. Protect and grow your hard-earned savings. To this end, we believe strongly that it's important that we eat our own cooking; we plan to allocate a significant percentage of our own net worth to Meridian Growth Fund.Performance Overview In our opinion, this disciplined process combined with decades of experience, extensive resources and a long-term investment horizon are the key ingredients required for consistent outperformance versus our peers and our benchmark. We look forward to many rewarding years stewarding your capital. The Meridian Growth Fund – Legacy Shares returned 17.31% during the twelve-month period ending June 30, 2014, underperforming its primary benchmark, the Russell 2500 Growth Index, which rose 26.26%. There were several factors that impacted performance during the period. The first was the portfolio manager transition that occurred on September 6, 2013. Prior to our portfolio management responsibilities, the portfolio underperformed the index by 4.12%. As part of the transition, we repositioned some of the portfolio's holdings to be consistent with our philosophy and process. The relative underperformance during the second half of the fiscal year ending June 30, 2014 was driven by the low-quality characteristics, such as low returns on capital, low profit margins and often negative earnings per share, of the stocks that performed best early in 2014. This underperformance was partially offset by the strong relative performance (seen in the low downside capture rates) during the market selloff from March to April 2014. The Meridian Growth Fund seeks to invest in high-quality (defined by overall profitability) and attractively valued stocks, which means the fund may underperform in periods such as the first quarter of this year. The second period of meaningful relative performance differential was the sell-off from the index's peak in the first week of March through the low in early April. During that time the fund captured just 70% of the market's decline, with the Russell 2500 Growth falling 9.17% and the fund falling 6.46%. This experience is consistent with our goal of capturing less downside than the market in turbulent, volatile environments. By putting risk and downside protection at the forefront of our process, we believe we will be better positioned to deliver strong long-term absolute and relative returns. The top contributors to performance during the period were Trimble Navigation (TRMB), Sensata Technologies (ST) and Cadence Design Systems (CDS). Trimble Navigation provides location-based solutions to its customers that enhance their productivity and profitability. The recovery in construction end markets and continued strong demand from the farm economy resulted in strong overall financial results for the company and a strong stock price. We trimmed the position as it began to exceed the upper end of the market cap range that we invest in. Sensata Technologies develops, manufactures and sells sensors and controls. We are attracted to the company's large growth opportunity, which is driven by increased sensor penetration in industries such as automobiles and general industrial opportunities. We find Sensata's business model to be attractive given the stability of its revenues, strong operating leverage and excellent management team. During the period, the company benefited from a rebound in European automobile sales and deployed capital in several small accretive acquisitions. We have been trimming the position modestly as the stock approaches our price target.Meridian Growth Fund performance Compass Minerals (CMP) is a leading producer of rock salt and specialty potash fertilizer. Its unique collection of resource assets has helped the company generate historically high returns on capital. We invested in Compass as we believed that earnings were due to turn after four years of weak road salt demand driven by mild Northeast winters and production problems at its potash mines. During 2013 the potash industry was rocked by the potential collapse of a European cartel, which led to falling potash prices. Facing significant uncertainty for the future of the potash market, we sold the stock.We continue to remain focused on individual stock selection and portfolio construction that identifies quality companies that we believe are experiencing temporary disruptions to their businesses. These disruptions enable us to buy the businesses at attractive prices and provide the portfolio with what we believe is an attractive risk-reward profile for our shareholders. Thank you for your continued investment in the Meridian Contrarian Fund. Jamie England, Larry Cordisco and Jim O'Connor Total Return Based on a $10,000 investment for the Period Ended June 30, 2014 Past performance is not predictive of future performance. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares and do not reflect the imposition of a 2% redemption fee on shares held 60 days or less to deter market timers. If reflected, the taxes and fees would reduce the performance quoted. Net asset value, investment return and principal value will fluctuate, so shares, when redeemed, may be worth more or less than their original cost. Read the rest of the Letter to Investors here: http://www.sec.gov/Archives/edgar/data/745467/000119312514330592/d763210dncsr.htm#tx763210_1

Should You Be Paying the 'Nanny Tax'? 3 Factors to Consider

Tuesday, September 9, 20143 Reasons to Buy the Financial Select Sector SPDR FundThe financial sector has had a pretty mediocre year so far, even as the S&P 500 (SNPINDEX: ^GSPC ) is up 8% and seems to hit a new record high every week. The Financial Select Sector SPDR Fund (NYSEMKT: XLF ) ETF is lagging the broad-based index by about a percentage point, and certain big names like Citigroup (NYSE: C ) have stalled or even dipped slightly. ^GSPC data by YCharts. However, there are a few reasons to like the banks and other financials over the long run. For starters, these companies are making tons of money, and most of the lingering effects of the financial crisis are finally being resolved. And many are trading for a nice discount to the value of their assets. Instead of picking individual stocks, perhaps the best way to invest here is to buy an ETF that tracks the sector. And the best financials ETF is the aforementioned Financial Select Sector SPDR Fund, which has the lowest expense ratio (just 0.16%) and the most assets under management among its peers. The fund tracks the Financial Select Sector Index, and its largest holdings are Berkshire Hathaway, Wells Fargo, JPMorgan Chase, Bank of America, and Citigroup. While history has shown that nothing in the stock market is a sure thing (especially in the financials sector), there are a few catalysts that could push the fund higher in the months and years to come. Crisis-related litigation may soon end at last However, one thing that has been ongoing -- and has even accelerated in recent years -- is the litigation expenses stemming from bad behavior leading up to the crisis. Most of this is working its way through the courts, and many banks are happy to pay billions to settle and put the financial crisis firmly in the past. The largest settlements have come from Bank of America and JPMorgan Chase, which settled lawsuits related to mortgage-backed securities for nearly $17 billion and $13 billion, respectively. And, most recently, Goldman Sachs settled its big lawsuit for $1.2 billion, which means all but three of the FHFA's 18 mortgage-related lawsuits have been settled. There are still pending lawsuits stemming from various financial-crisis issues, but for the most part, the "big ones" are done with. When there is legal drama surrounding a company, it creates uncertainty that can depress the stock price. This is especially true when you're dealing with lawsuits of this magnitude. After all, when a company might have to pay somewhere between $4 billion and $20 billion to settle a case, the ultimate impact on the company's balance sheet can vary widely based on the outcome of the settlement. M&A and IPO activity could continue to rise In fact, the Alibaba group is finally about to complete its long-anticipated IPO, which should be the largest in history. And this is after an already active 2014, in which we've seen large companies like GoPro and El Pollo Loco go public. So long as the market stays hot, we could see this level of activity continue or even improve as companies see the potential to receive excellent value for their offerings as they go public. During the second quarter, pretty much all banks with investment banking divisions saw equity underwriting revenue pop. And the combination of a hot market and low interest rates should keep M&A activity high, which is also an excellent driver of advisory revenue for the banks. For example, JPMorgan Chase, the No. 1 investment bank in the U.S. in terms of fee revenue, saw its revenue from advisory fees rise by 31% year over year in the second quarter. It's not a sure thing, but the upside outweighs the risk As you can see, the "big four" banks, which combine for about 27% of the fund's holdings, trade very cheaply relative to their book values, both on a historical basis and on an absolute basis. And some banks, such as Citigroup and Bank of America, actually trade for substantially less than their book value. Basically, this makes me believe there is more upside potential than downside risk here. No matter what the market does, the value of the assets of these companies will serve to buoy the stock price in tough times, and those very assets will make the companies money in good times. Richard Pzena, founder of Pzena Investment Management, even estimates that bank earnings could even double over the next few years, and in the meantime you can collect a 7%-8% return on assets, which you're already buying at a discount. So, while there are no guarantees, especially with a correction being called for and a lot of legacy assets still on the banks' balance sheets, there are some compelling reasons to like the financial sector right now. Are these dividend stocks an even better investment than ETFs? Thursday, September 4, 2014Is Apple About To Jolt The Smartphone Market?

On September 9, Apple (AAPL) will unveil a series of new premium-range products – one being the much awaited iPhone6 with a big screen. Amid intense competition, it is being highly expected that Apple will carve its mark in a new style. Let's check out what is in store for the smartphone market at the Apple event scheduled the coming week. iPhone specs are all in rumors Apple is expected to release the iPhone 6 with a much larger screen than iPhone 5 and 5s series which have already captured the minds of several Apple fans. The iPhone might have a 4.7-inch screen making it more competitive with the present Google (GOOG) Android phone and the Samsung (SSNLF) Galaxy Tab. There are also speculations that there might be another iPhone 6 variant with a 5.5-inch screen. It is being assumed that a large screen will unleash a surge in sales for Apple's upcoming iPhone among those who already own models in the existing range of Apple iPhones. Analysts have opined that Apple would probably sell at least 70 million units of this new iPhone within months of its entry into the market. Latest rumors speak of the new iPhone being sleeker with a lighter chassis than the present iPhone 5s. It would probably have edge to edge display and the design might look like an iPad mini. To improve the durability of iPhone 6, the chassis would be made of Liquidmetal, a material for which Apple holds exclusive rights. Liquidmetal is extremely strong and durable and even when used in minute quantities gives the build quality as achieved by using aluminum. Also, to keep rival agape, news sources have confirmed the use of sapphire glass for the screen which makes it almost scratch free and "nearly indestructible." Indeed, Apple has built a new plant in Arizona which manufactures sapphire glass. Though the same material is used in iPhone 5s's Touch ID Home button and cover of the rear-facing camera, Apple does have plans of using this glass largely for the new iPhone as it has spent around $578 million on a deal with GT Technology to speed up the development of the sapphire glass displays destined for the iPhone 6. Also the operating system would stand updated to i

Subscribe to:

Comments (Atom)

|

) reported its second quarter earnings, posting higher revenues and flat earnings compared to last year’s Q2 results.

) reported its second quarter earnings, posting higher revenues and flat earnings compared to last year’s Q2 results.

Michael Tullberg/Getty Images Los Angeles County's fabled Sunset Strip -- home to numerous legendary nightclubs -- is going corporate. Goodbye, Rat Pack and Guns N' Roses; hello, Marriott International (MAR). Gangsters and Guitarists Through a quirk of urban planning, the Strip -- a 1.6-mile stretch of Sunset Boulevard -- was part of unincorporated land within Los Angeles city limits (these days, it belongs to the micro-city of West Hollywood). As such, it was overseen not by the L.A. Police Department, but by the more lax County Sheriff's department. Entrepreneurs took advantage of this, and in the early 20th century the Strip soon became the hottest entertainment destination in the L.A. area, home to clubs, bars and the occasional house of ill repute. In the 1940s and 1950s its nightclubs frequently hosted the top stars of the era. Many a band across the subsequent decades rose to prominence playing joints like The Roxy, Whisky A Go Go (still going strong at 50), and the Viper Room. Throughout the world, the Strip was nearly synonymous with nightlife. So much so that, according to some, its name was cribbed by the burgeoning city of Las Vegas to title the strategic section of its main thoroughfare. For many years now, the heart of Las Vegas Boulevard has been known simply as "The Strip." The City That Sometimes Sleeps The Strip is not the only game in town for visitors. Close by is the gay mecca of West Hollywood's "Boy's Town" neighborhood, while the tiny city's location in the kernel of L.A. makes it the perfect springboard for visiting Hollywood, L.A.'s beaches, and the neighboring Beverly Hills. Tourism is big business for West Hollywood. Twenty percent of the municipality's fiscal 2013 take came from the transient occupancy (i.e., lodging) taxes levied on those visitors. This brought in a cool $18 million that year -- 18 percent higher year over year, by the way -- making it WeHo's No. 2 revenue source. And there's more where that came from. Last year, West Hollywood hotels collectively had an occupancy rate of 82 percent, according to industry watcher STR. This is much higher than the 2013 national figure of 62 percent, as calculated by the American Hotel & Lodging Association -- indicating that there's plenty of room for growth. Here Come the Hoteliers So it's no surprise to learn that some big names in the sector are very interested in West Hollywood, and where better to build than its famous street? A host of hotel projects on the Strip are in various stages of development. Developer CIM Group has cleared a pair of parcels on either side of the intersection of busy La Cienega Boulevard and the Strip. One is to be home to the 286-room four-star James Los Angeles hotel, comprised of a pair of 10-story towers. The other parcel will be the site of residential buildings. Meanwhile, across the street from The Roxy, the sun will rise on an Edition Hotel, Marriott International's boutique brand. The company plans to construct an Edition boasting nearly 200 rooms, which should open in 2017. Marriott has partnered with industry veteran Ian Schrager on the Edition line. Schrager is a co-founder of Morgans Hotel Group (MHGC), and that company's flagship Southern California property is the Strip's Mondrian Hotel. The Last Encore? The wave of hotels threatens to obliterate the Strip's smaller businesses, which include some places that give the stretch its character and reputation. According to Bloomberg, a division of engineering company AECOM Technology (ACM) is aiming to build a complex on the eastern end of the Strip anchored by a 149-room hotel. At the moment, that land is occupied by the local iteration of Live Nation's (LYV) House of Blues concert hall chain. According to a spokesman for the club, it is finding a new location. The building itself will probably suffer the fate of the Strip's first theater, the nearly 50-year old Tiffany. That venue was razed by CIM Group last year to make way for its La Cienega project. That seems to be the trajectory of the neighborhood -- fun stuff out, lodgings in. Across the street from Whisky A Go Go lies the Hustler Store, the main retail outlet of the notorious porn empire. Like House of Blues, it's packing up and moving elsewhere. In the Bloomberg article, a West Hollywood Community Development Department official speculated on what the future of the building could be. It might, he mused, be torn down to be replaced by -- yep -- a new hotel project. More from Eric Volkman

Michael Tullberg/Getty Images Los Angeles County's fabled Sunset Strip -- home to numerous legendary nightclubs -- is going corporate. Goodbye, Rat Pack and Guns N' Roses; hello, Marriott International (MAR). Gangsters and Guitarists Through a quirk of urban planning, the Strip -- a 1.6-mile stretch of Sunset Boulevard -- was part of unincorporated land within Los Angeles city limits (these days, it belongs to the micro-city of West Hollywood). As such, it was overseen not by the L.A. Police Department, but by the more lax County Sheriff's department. Entrepreneurs took advantage of this, and in the early 20th century the Strip soon became the hottest entertainment destination in the L.A. area, home to clubs, bars and the occasional house of ill repute. In the 1940s and 1950s its nightclubs frequently hosted the top stars of the era. Many a band across the subsequent decades rose to prominence playing joints like The Roxy, Whisky A Go Go (still going strong at 50), and the Viper Room. Throughout the world, the Strip was nearly synonymous with nightlife. So much so that, according to some, its name was cribbed by the burgeoning city of Las Vegas to title the strategic section of its main thoroughfare. For many years now, the heart of Las Vegas Boulevard has been known simply as "The Strip." The City That Sometimes Sleeps The Strip is not the only game in town for visitors. Close by is the gay mecca of West Hollywood's "Boy's Town" neighborhood, while the tiny city's location in the kernel of L.A. makes it the perfect springboard for visiting Hollywood, L.A.'s beaches, and the neighboring Beverly Hills. Tourism is big business for West Hollywood. Twenty percent of the municipality's fiscal 2013 take came from the transient occupancy (i.e., lodging) taxes levied on those visitors. This brought in a cool $18 million that year -- 18 percent higher year over year, by the way -- making it WeHo's No. 2 revenue source. And there's more where that came from. Last year, West Hollywood hotels collectively had an occupancy rate of 82 percent, according to industry watcher STR. This is much higher than the 2013 national figure of 62 percent, as calculated by the American Hotel & Lodging Association -- indicating that there's plenty of room for growth. Here Come the Hoteliers So it's no surprise to learn that some big names in the sector are very interested in West Hollywood, and where better to build than its famous street? A host of hotel projects on the Strip are in various stages of development. Developer CIM Group has cleared a pair of parcels on either side of the intersection of busy La Cienega Boulevard and the Strip. One is to be home to the 286-room four-star James Los Angeles hotel, comprised of a pair of 10-story towers. The other parcel will be the site of residential buildings. Meanwhile, across the street from The Roxy, the sun will rise on an Edition Hotel, Marriott International's boutique brand. The company plans to construct an Edition boasting nearly 200 rooms, which should open in 2017. Marriott has partnered with industry veteran Ian Schrager on the Edition line. Schrager is a co-founder of Morgans Hotel Group (MHGC), and that company's flagship Southern California property is the Strip's Mondrian Hotel. The Last Encore? The wave of hotels threatens to obliterate the Strip's smaller businesses, which include some places that give the stretch its character and reputation. According to Bloomberg, a division of engineering company AECOM Technology (ACM) is aiming to build a complex on the eastern end of the Strip anchored by a 149-room hotel. At the moment, that land is occupied by the local iteration of Live Nation's (LYV) House of Blues concert hall chain. According to a spokesman for the club, it is finding a new location. The building itself will probably suffer the fate of the Strip's first theater, the nearly 50-year old Tiffany. That venue was razed by CIM Group last year to make way for its La Cienega project. That seems to be the trajectory of the neighborhood -- fun stuff out, lodgings in. Across the street from Whisky A Go Go lies the Hustler Store, the main retail outlet of the notorious porn empire. Like House of Blues, it's packing up and moving elsewhere. In the Bloomberg article, a West Hollywood Community Development Department official speculated on what the future of the building could be. It might, he mused, be torn down to be replaced by -- yep -- a new hotel project. More from Eric Volkman

Getty Images Whether it's for child care, lawn work or a host of other chores, millions of Americans hire people and bring them into their homes to do necessary work. But many people don't realize that doing so leaves themselves open to a potential tax liability, nicknamed the nanny tax. Let's take a closer look. 1. You Can Pay Up to Certain Amounts Without Triggering Nanny Tax The nanny tax is designed to ensure that your household employees get credit for their work for purposes of Social Security, Medicare and unemployment benefits. As a result, the rules governing when the Internal Revenue Service collects the nanny tax track the income thresholds for various features of those programs. Specifically, if you pay cash wages of $1,900 or more, then you have to pay Social Security and Medicare taxes of 15.3 percent. You're allowed to withhold half of that amount from what you pay your household employee, just as Social Security and Medicare taxes are withheld from most paychecks. Similarly, if you pay a household employee $1,000 or more in any calendar quarter, then you'll owe 6 percent in federal unemployment tax on up to $7,000 in annual wages. 2. Hiring Kids Under 18 Can Save You a Lot of Trouble The nanny tax can be a huge hassle when you hire household employees, but there are some exceptions even if you pay more than the threshold amounts above. Paying members of your own family lets you take advantage of more lenient rules. If you pay your spouse or your under-21 child to do any household work, then any pay isn't treated as wages subject to the nanny tax. A more common way to avoid the nanny tax is to hire babysitters, lawn-care providers and others under the age of 18. As long as the employee isn't primarily in the business of providing those services -- such as being a student in school at the same time -- then you won't have to pay the nanny tax on those wages even if they exceed the $1,900 limit. However, the unemployment-tax component of the nanny tax isn't subject to the under-18 rule. So if you pay more than $1,000 in a quarter, it doesn't matter that the person is under 18 -- you still have to deal with the tax. 3. Using a Contractor -- Not an Employee -- Can Save You Money The nanny tax only applies to those who qualify as employees as opposed to independent contractors. Although the distinction can be complicated, the primary way to understand when someone is an employee is to focus on the degree of control you have over their work. If you have control not just what type of work is done but also the specific way the worker does it, then you're more likely to have an employee. On the other hand, if you merely say you want a task done but leave the details to the worker, that resembles an independent contractor relationship more closely. In addition, if the worker provides tools and equipment rather than relying on you for them, that's another sign of a contractor relationship. Properly classifying a worker is essential. If your worker isn't an employee, then you don't owe the nanny tax, as the worker is responsible for any self-employment taxes from earnings. But if the IRS disagrees with your characterization, then you can end up having to pay interest and penalties. The nanny tax isn't generally a huge burden financially, but it can come as a surprise if you're not prepared for it. By being aware of when the nanny tax applies, you can take steps to avoid it and save yourself some money as a result. More from Dan Caplinger

Getty Images Whether it's for child care, lawn work or a host of other chores, millions of Americans hire people and bring them into their homes to do necessary work. But many people don't realize that doing so leaves themselves open to a potential tax liability, nicknamed the nanny tax. Let's take a closer look. 1. You Can Pay Up to Certain Amounts Without Triggering Nanny Tax The nanny tax is designed to ensure that your household employees get credit for their work for purposes of Social Security, Medicare and unemployment benefits. As a result, the rules governing when the Internal Revenue Service collects the nanny tax track the income thresholds for various features of those programs. Specifically, if you pay cash wages of $1,900 or more, then you have to pay Social Security and Medicare taxes of 15.3 percent. You're allowed to withhold half of that amount from what you pay your household employee, just as Social Security and Medicare taxes are withheld from most paychecks. Similarly, if you pay a household employee $1,000 or more in any calendar quarter, then you'll owe 6 percent in federal unemployment tax on up to $7,000 in annual wages. 2. Hiring Kids Under 18 Can Save You a Lot of Trouble The nanny tax can be a huge hassle when you hire household employees, but there are some exceptions even if you pay more than the threshold amounts above. Paying members of your own family lets you take advantage of more lenient rules. If you pay your spouse or your under-21 child to do any household work, then any pay isn't treated as wages subject to the nanny tax. A more common way to avoid the nanny tax is to hire babysitters, lawn-care providers and others under the age of 18. As long as the employee isn't primarily in the business of providing those services -- such as being a student in school at the same time -- then you won't have to pay the nanny tax on those wages even if they exceed the $1,900 limit. However, the unemployment-tax component of the nanny tax isn't subject to the under-18 rule. So if you pay more than $1,000 in a quarter, it doesn't matter that the person is under 18 -- you still have to deal with the tax. 3. Using a Contractor -- Not an Employee -- Can Save You Money The nanny tax only applies to those who qualify as employees as opposed to independent contractors. Although the distinction can be complicated, the primary way to understand when someone is an employee is to focus on the degree of control you have over their work. If you have control not just what type of work is done but also the specific way the worker does it, then you're more likely to have an employee. On the other hand, if you merely say you want a task done but leave the details to the worker, that resembles an independent contractor relationship more closely. In addition, if the worker provides tools and equipment rather than relying on you for them, that's another sign of a contractor relationship. Properly classifying a worker is essential. If your worker isn't an employee, then you don't owe the nanny tax, as the worker is responsible for any self-employment taxes from earnings. But if the IRS disagrees with your characterization, then you can end up having to pay interest and penalties. The nanny tax isn't generally a huge burden financially, but it can come as a surprise if you're not prepared for it. By being aware of when the nanny tax applies, you can take steps to avoid it and save yourself some money as a result. More from Dan Caplinger